Global investors find reason for optimism in China's financial market

Since July, China's markets have rallied, thanks to relative optimism among domestic and foreign investors about the country's economic outlook.

The success of the nation's epidemic prevention work is partially credited for the market confidence. China is recovering quicker from the coronavirus outbreak than the rest of the world, with the orderly resumption of work an example for others to follow.

China's continuous financial reforms in recent years have laid the foundation for foreigners to further participate in the economy, providing them with better access and ownership and offering greater operational efficiency.

Even during the first half of the year when the coronavirus was disrupting the economy, the pace of reforms did not slow down.

A rare bright spot amid upheaval

The effective epidemic prevention and relative optimistic economic outlook have led to a growing appetite for Chinese stocks among both domestic and overseas investors.

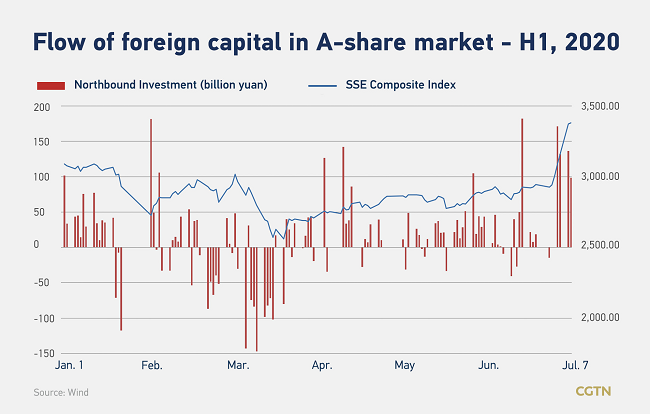

The Shanghai Composite Index surged by 15.61 percent in the first seven trading days of July. Net inflows of overseas investment through the Shanghai-Hong Kong and Shenzhen-Hong Kong Stock Connect programs have piled up since late March, when the epidemic situation in China was turning to controllable and stable.

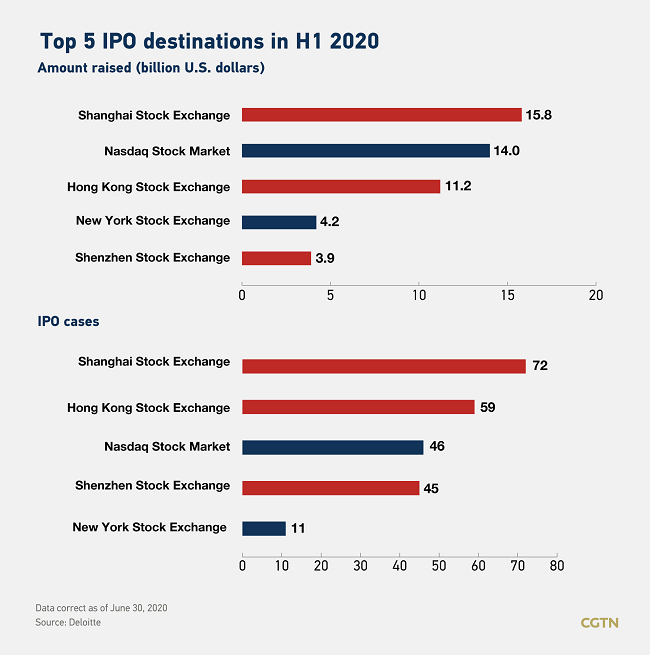

Regarding the initial public offering (IPO) scene, the epidemic slowed down global IPOs in the first half of the year, a total of 412 companies were listed and funds worth 66.7 billion U.S. dollars were raised, down 20 percent year on year.

However, IPOs continued to grow in the Chinese mainland and Hong Kong, accounting for 43 and 46 percent of the world's total by deal numbers and proceeds respectively.

The Shanghai Stock Exchange topped both IPO amount raised and cases in the first half of the year.

On the macro level, China is the only major economy forecast to grow this year. A one-percent growth seems encouraging when the United States and the European Union are expected to contract by eight percent and 10.2 percent respectively, data from the International Monetary Fund showed at the end of June. The organisation also projected China will record the strongest rebound next year.

Reforms pave way for market exuberance

Apart from faster recovery from COVID-19, a more intrinsic factor for the market exuberance is the country's continuous financial reforms over recent years and during the outbreak, which have laid foundations to embrace more overseas participants especially in aspects such as market mechanisms, IPO systems, foreign access and ownership.

For example, China in March announced it is bringing forward the planned opening of its capital market by eight months, ending ownership limits for foreign investors in securities, futures, and insurance business.

Japanese investment bank Nomura Holdings Inc. pioneered to set up a securities joint venture in Shanghai, which is the first newly established foreign-controlled brokerage on the Chinese mainland under the new regulations. J.P. Morgan Futures Co., Ltd. became the country's first wholly foreign-owned futures trading firm.

In May, China decided to scrap quota restrictions on the Qualified Foreign Institutional Investors (QFII) program and its yuan-denominated sibling, RQFII, in a bid to further widen the investment scope for overseas investors.

Fuel for further reforms

The virus and geopolitical tensions with the U.S. have accelerated China's financial reforms to counter uncertainties. Concern over Chinese firms' reliance on U.S. markets for fundraising is driving action to increase the allure of homegrown bourses.

Against the backdrop of Washington's scrutiny and delisting-threatening bill, big Chinese companies listed in the U.S. have started considering secondary listings in Hong Kong.

In June, e-commerce giant JD.com Inc. and online game company NetEase Inc. carried out secondary offering in Hong Kong, after e-commerce conglomerate Alibaba Group pioneered the practice in November last year under the new listing rules of the city, along with weighted voting right regime.

Experts said the recent "homecoming" cases are just the beginning of the story, adding that the trend will last for a couple of years due to continuous financial reforms in China and external factors.

Amid such trend, the question about whether Shanghai can be the new home they desire is getting new attention.

"The development of the financial market in Shanghai is very good, but in general, it is not really international yet," said Zhou Xiaochuan, China's former central bank governor, in a video speech in the Lujiazui Forum of top financial regulators in Shanghai.

"If China is determined to achieve substantial development in this area, it must focus on internationalization, strengthening international cooperation, and building Shanghai into a center with more international institutions and much improved capital transactions," Zhou said.

There are plenty of Chinese companies of high quality, and companies and regulators are willing to push forward further changes, he said. "But there is also a process to gradually improve corporate governance and raise companies' awareness of improving accounting and auditing practice."